I’ve been asked to put this piece, part of IKN339, onto the blog. So here it is.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Guest

Article by reader BW: “Lifting the Dress on All In Sustaining Costs”

Article by reader BW: “Lifting the Dress on All In Sustaining Costs”

(Alt. title “How things can grow

out of virtually nothing when you run a blog”)

out of virtually nothing when you run a blog”)

First a

little background: In the last couple of weeks over at the blog, both myself

and reader ‘BW’ have been playing on the theme of All In Sustaining Costs

(AISC). It’s one of those subjects that’s itched at me for a while, because it

doesn’t need much numbercrunching to see that AISC is a neat new way of

spinning costs figures, rather than a useful metric that applies to all mining

companies equally. Thing is, I haven’t really got round to throwing darts at

AISC (even after being egged on by a couple of friends on more than one

occasion) but then a couple of weeks ago I broke the ice with a very simple

post and observation, it turned out to be the way in.

little background: In the last couple of weeks over at the blog, both myself

and reader ‘BW’ have been playing on the theme of All In Sustaining Costs

(AISC). It’s one of those subjects that’s itched at me for a while, because it

doesn’t need much numbercrunching to see that AISC is a neat new way of

spinning costs figures, rather than a useful metric that applies to all mining

companies equally. Thing is, I haven’t really got round to throwing darts at

AISC (even after being egged on by a couple of friends on more than one

occasion) but then a couple of weeks ago I broke the ice with a very simple

post and observation, it turned out to be the way in.

It all started on October 28th

and my post “Understanding “All In Sustaining Costs”, Detour Gold (DGC.to) edition”, which as a missive was

simplicity itself and to shed light on the “virtually nothing” sub-header above

I’ll even tell you how it all happened. That day I was about 30 minutes early

for an appointment in Lima and feeling a little drained after a long day, so I

decided to pause for a coffee in a nearby Starbucks. While there it just so

happened that the DGC 3q15 financials NR was published, I picked up the

corporate NR on my (rather basic HP) tablet and, amused at the spin they gave

the numbers, tapped out the straightforward post seen that day on the virtual

keyboard. I didn’t look at the SEDAR filings at all, it took about 15 minutes

start to finish, I hit Send, finished my latte and went to the meeting. By way

of a reminder, here’s the main numbery bit of that post:

and my post “Understanding “All In Sustaining Costs”, Detour Gold (DGC.to) edition”, which as a missive was

simplicity itself and to shed light on the “virtually nothing” sub-header above

I’ll even tell you how it all happened. That day I was about 30 minutes early

for an appointment in Lima and feeling a little drained after a long day, so I

decided to pause for a coffee in a nearby Starbucks. While there it just so

happened that the DGC 3q15 financials NR was published, I picked up the

corporate NR on my (rather basic HP) tablet and, amused at the spin they gave

the numbers, tapped out the straightforward post seen that day on the virtual

keyboard. I didn’t look at the SEDAR filings at all, it took about 15 minutes

start to finish, I hit Send, finished my latte and went to the meeting. By way

of a reminder, here’s the main numbery bit of that post:

Detour Gold (DGC.to) just reported its 3q15 and here’s my

favourite bit:

favourite bit:

Gold sold: 126,241 oz

Average realized price per Oz Au: U$1,164

All In Sustaining Cost per Oz Au: U$1,071

Difference between two: U$93/oz

Total revenue difference: + U$11.74m

Net loss: US$44.3m

Adjusted net loss:U$13.3m

Hey, d’ya think that All In Sustaining Cost might not mean what you thought it

meant? Perhaps?

It was meant as a quick snark-shot

and I thought nothing else of it until a couple of days later when ‘BW’ (whose

ID will remain out the public eye but I will say he’s an excellent financials

person who’s modest to a fault about his undoubted ability) wrote in with the

mail that became this post “Great feedback on the Detour Gold (DGC.to)”

which took my basic idea on DGC and ran a lot further with it (it was very well

done too, I recommend a (re) read).

and I thought nothing else of it until a couple of days later when ‘BW’ (whose

ID will remain out the public eye but I will say he’s an excellent financials

person who’s modest to a fault about his undoubted ability) wrote in with the

mail that became this post “Great feedback on the Detour Gold (DGC.to)”

which took my basic idea on DGC and ran a lot further with it (it was very well

done too, I recommend a (re) read).

From there and with all thanks to

BW, the idea was lodged in my mind and last week I ran a couple of posts, the

first one called “More “All In Sustaining Costs” baloney, Primero Mining (P.to) (PPP) edition” which was

basically the same as the DGC idea but applied to Primero, then finally on

November 4th there was the post “Having your cake and eating it” which covered in conceptual style the reason why

Deprecation Depletion and Amortization (DD&A) is important to include in

operating costs models.

BW, the idea was lodged in my mind and last week I ran a couple of posts, the

first one called “More “All In Sustaining Costs” baloney, Primero Mining (P.to) (PPP) edition” which was

basically the same as the DGC idea but applied to Primero, then finally on

November 4th there was the post “Having your cake and eating it” which covered in conceptual style the reason why

Deprecation Depletion and Amortization (DD&A) is important to include in

operating costs models.

Now for

the good news: Due to those last two amateurish efforts on my part, ‘BW’ wrote in

again late last week and expanded a little on his original comments about

Detour Gold (DGC.to), but this time taking Primero Mining (PPP) (P.to) as his

example (and quarry). While his mail was obviously meant for my eyes and

education, it was so good I asked him on Friday evening if he would let me run

his mail as a Guest Article in this Sunday’s edition of The IKN Weekly. He

kindly agreed and here we are, though he did insist that I add that his piece

is a simple proxy for other metrics, e.g. EBITDA. The purpose behind his mail

was to get ME (not anyone else) to apply it to show the true production costs

of any given miner (not just his example of Primero) from the data published in

an income statement. But me, I’m keen to let as many people as possible benefit

from BW’s smarts on this subject which is why I asked BW if he’d let me run it

here (some very slight editing and formatting done, but it’s really as-is).

Therefore without further ado here’s BW:

the good news: Due to those last two amateurish efforts on my part, ‘BW’ wrote in

again late last week and expanded a little on his original comments about

Detour Gold (DGC.to), but this time taking Primero Mining (PPP) (P.to) as his

example (and quarry). While his mail was obviously meant for my eyes and

education, it was so good I asked him on Friday evening if he would let me run

his mail as a Guest Article in this Sunday’s edition of The IKN Weekly. He

kindly agreed and here we are, though he did insist that I add that his piece

is a simple proxy for other metrics, e.g. EBITDA. The purpose behind his mail

was to get ME (not anyone else) to apply it to show the true production costs

of any given miner (not just his example of Primero) from the data published in

an income statement. But me, I’m keen to let as many people as possible benefit

from BW’s smarts on this subject which is why I asked BW if he’d let me run it

here (some very slight editing and formatting done, but it’s really as-is).

Therefore without further ado here’s BW:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Lifting The Dress on All

In Sustaining Costs

In Sustaining Costs

By ‘BW’

Prompted by your piece on Primero as

well as your response to a reader’s question regarding the “importance” of

considering DD&A, you have provoked me to offer you consolidation of my

thoughts regarding AISC and its noble goal to offer transparency, a.k.a.

eloquent obfuscation, to the market (excerpt below from my database).

Well, lifting up that dress a bit more, we could consider AIC, but taxes, debt

service, and dividends are not included there. It baffles the mind why

these items are not considered a part of a company’s sustainability. I

reckon we don’t want to pull that dress up any higher for fear of what is

beneath!

well as your response to a reader’s question regarding the “importance” of

considering DD&A, you have provoked me to offer you consolidation of my

thoughts regarding AISC and its noble goal to offer transparency, a.k.a.

eloquent obfuscation, to the market (excerpt below from my database).

Well, lifting up that dress a bit more, we could consider AIC, but taxes, debt

service, and dividends are not included there. It baffles the mind why

these items are not considered a part of a company’s sustainability. I

reckon we don’t want to pull that dress up any higher for fear of what is

beneath!

Since you are one of the few who

unabashedly exposes the BS out there concerning the mining industry, at the

risk of being presumptuous, below I offer some suggestions as well as make some

other observations.

unabashedly exposes the BS out there concerning the mining industry, at the

risk of being presumptuous, below I offer some suggestions as well as make some

other observations.

In the case of Primero, for Q3,

sales were 71,417AuEq oz for which revenues were $1,109/AuEq oz (low because

they have 2 streaming deals, which can’t be conveniently buried somewhere)

sales were 71,417AuEq oz for which revenues were $1,109/AuEq oz (low because

they have 2 streaming deals, which can’t be conveniently buried somewhere)

1.

AISC = $775/AuEq oz (includes $87/AuEq oz for G&A, marginally high at

11%)

AISC = $775/AuEq oz (includes $87/AuEq oz for G&A, marginally high at

11%)

2.

Finance charges = $43/AuEqoz

Finance charges = $43/AuEqoz

3.

Other (assumed not in AISC) = $75/AuEqoz

Other (assumed not in AISC) = $75/AuEqoz

4.

Taxes = $243/AuEqoz

Taxes = $243/AuEqoz

Subtotal: $1,136/AuEq oz (i.e. cash

outlays)

outlays)

5.

DD&A = $273/AuEq oz

DD&A = $273/AuEq oz

Subtotal: $1,409/AuEqoz (i.e. cash

outlays + past cash outlays, of which only some sustaining capital was

accounted for previously)

outlays + past cash outlays, of which only some sustaining capital was

accounted for previously)

6.

5.75% Debenture = $82/AuEq oz ($75M over 38

months, so $5.921M/Q) – 38 months is earliest redemption date, which can occur

up to 62 months

5.75% Debenture = $82/AuEq oz ($75M over 38

months, so $5.921M/Q) – 38 months is earliest redemption date, which can occur

up to 62 months

Subtotal: $1,491/AuEq oz (i.e. cash

outlays + past cash outlays, of which only some sustaining capital was

accounted for previously + future outlays)

outlays + past cash outlays, of which only some sustaining capital was

accounted for previously + future outlays)

7.

Mark-to-Market = negative $126/AuEq oz (if debenture is amortized

and applied to cost, which is only fair to include)

Mark-to-Market = negative $126/AuEq oz (if debenture is amortized

and applied to cost, which is only fair to include)

Final

total $1,365/AuEq oz (i.e. what it really costs Primero to produce an ounce of

gold or gold equivalent).

total $1,365/AuEq oz (i.e. what it really costs Primero to produce an ounce of

gold or gold equivalent).

They also have some equipment

leases, but appear to add only incremental cost on a per-Q basis and therefore

not included.

leases, but appear to add only incremental cost on a per-Q basis and therefore

not included.

They have $43.1M in cash, but $30.4M

in payables – net cash = $12.7M.

in payables – net cash = $12.7M.

They must pay off $49.684M for 6.75%

Brigus debenture by March, 2016, which I suspect that they will do with shares.

Brigus debenture by March, 2016, which I suspect that they will do with shares.

But no worries – they have a $75M

credit line. (otto note: I laughed

hard at BW’s dry sense of humour here).

credit line. (otto note: I laughed

hard at BW’s dry sense of humour here).

Finally, another note on Cash Flow

Models (CFM) as applied to new projects and acquisitions. Once the project

starts construction and/or is acquired, the investor focuses on margins, i.e.,

FCF; the NPV becomes irrelevant, but investors want to see the “profit” earned

from the outlays. The CFMs are not updated for any financing for public

purview; I have never seen a “forensic” pre-project/acquisition review

available to the public. If there is debt on the project, this review

essentially occurs every quarter in order to determine compliance with regard

to covenants, but only general statements are made to the public regarding

covenant compliance. This only points out that there is no “means test” in

the public domain for the copious use of the word “accretive”.

Models (CFM) as applied to new projects and acquisitions. Once the project

starts construction and/or is acquired, the investor focuses on margins, i.e.,

FCF; the NPV becomes irrelevant, but investors want to see the “profit” earned

from the outlays. The CFMs are not updated for any financing for public

purview; I have never seen a “forensic” pre-project/acquisition review

available to the public. If there is debt on the project, this review

essentially occurs every quarter in order to determine compliance with regard

to covenants, but only general statements are made to the public regarding

covenant compliance. This only points out that there is no “means test” in

the public domain for the copious use of the word “accretive”.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IKN339 back and sincere thanks

again to BW for first taking the time and effort to write to me, then allowing

me to publish his musings to a wider audience. I’m fully aware that he

considers them basic and ballpark (especially compared to what he usually does)

but I also know that this type of insight is greatly appreciated by at least

some of the IKN audience.

again to BW for first taking the time and effort to write to me, then allowing

me to publish his musings to a wider audience. I’m fully aware that he

considers them basic and ballpark (especially compared to what he usually does)

but I also know that this type of insight is greatly appreciated by at least

some of the IKN audience.

As well as BW’s model on Primero,

which shows just why the company recorded a net loss of 3c/share despite

claiming to have an AISC of $775/oz, I liked the last paragraph which looks at

the question reader ‘DB’ asked me in the have-cake-eat-it post from a different

and better angle. Again, if any given company had no debt (in real terms, we

shouldn’t fret too much about payables as long as there are receiveable and/or

cash to cover them) and had already raised all its required capex from the sale

of equities (placements etc), fundies theory states that the company’s

operational profitability, not just its net profitability will reflect directly

in its share price. But when debt gets in the way it needs to be serviced from

somewhere, then eventually principle needs to be paid off from somewhere and

that doesn’t just happen from money created out of thin air.

which shows just why the company recorded a net loss of 3c/share despite

claiming to have an AISC of $775/oz, I liked the last paragraph which looks at

the question reader ‘DB’ asked me in the have-cake-eat-it post from a different

and better angle. Again, if any given company had no debt (in real terms, we

shouldn’t fret too much about payables as long as there are receiveable and/or

cash to cover them) and had already raised all its required capex from the sale

of equities (placements etc), fundies theory states that the company’s

operational profitability, not just its net profitability will reflect directly

in its share price. But when debt gets in the way it needs to be serviced from

somewhere, then eventually principle needs to be paid off from somewhere and

that doesn’t just happen from money created out of thin air.

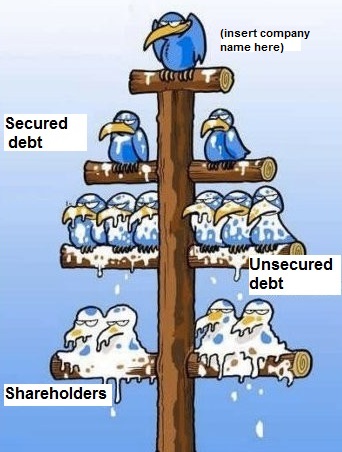

When you (the investor) buy a

share, you buy a part of the equity of the company in question. The definition

of “equity” is straightforward, it’s “assets minus liabilities”. Therefore if

your company’s main fixed asset is non-renewable, e.g. a mine with valuable

rock that you pound into bits for its metal content, when the metal’s gone so

is all the fixed asset value. The only thing you’re going to have left is the

cash you generated from all that mining activity, minus any debt on the books.

Therefore it stands to reason that if you use all (or even most) of the cash

you generate to pay off the debt holders, there’s going to be precious little

left for the people holding the shares at the end. No distributions, no

dividends, no soup for you.

share, you buy a part of the equity of the company in question. The definition

of “equity” is straightforward, it’s “assets minus liabilities”. Therefore if

your company’s main fixed asset is non-renewable, e.g. a mine with valuable

rock that you pound into bits for its metal content, when the metal’s gone so

is all the fixed asset value. The only thing you’re going to have left is the

cash you generated from all that mining activity, minus any debt on the books.

Therefore it stands to reason that if you use all (or even most) of the cash

you generate to pay off the debt holders, there’s going to be precious little

left for the people holding the shares at the end. No distributions, no

dividends, no soup for you.

Which is why I love this cartoon so

very much and use it on the blog when given a legitimate opportunity.

very much and use it on the blog when given a legitimate opportunity.