Gold

versus silver (from IKN369, dated June 5th)

Now for the second question posed

by KM, which goes like this:

high? Isn’t the physical prevalence of silver over gold in the earth reflect a

much lower ratio? Also, my understanding is that the industrial demand usage

will increase over time… I am especially interested in the increasing usage of

silver in purification and medicine.

The more I put thought to it, the

more I saw it as a good question that deserves an extended answer rather than one

of my all-too typical and lazy three line specials. It’s one of the issues we

as precious metals investors have in the corner of our eyes but it tends not to

be addressed correctly and can fall prey to hype and soapbox-spouting on either

side of the debate. To answer KM is to explain why gold stocks are, in my considered

opinion, a better bet in the near and long term than anything predominantly

silver and for that reason the whole issue expanded into this rather different

main section today; I want to lay my position on the line.

that promote silver as a better bet than gold, with one of the principle ones

the “physics arguments” alluded to by KM in his question. They’ve recently been

getting a revival, thanks at least in part to statements made by First

Majestic’s (FR.to) (AG) CEO Keith Neumeyer who seems to be framing himself as a

champion of the silverbug cause. The first ones states that the true silver to

gold ratio in the earth’s crust, now generally accepted by the egghead

scientists that study these things, is 16X. That’s to say for every ounce of

gold in the earth’s crust there are sixteen ounces of silver. Therefore the

argument goes that eventually the price of silver will be one sixteenth of the

price of gold because the value will eventually reflect the relative levels of

abundance. The logic of this argument may be simple, but it’s also sensible

enough at first sight.

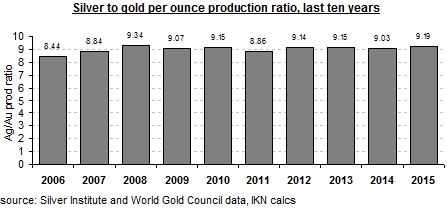

The second aspect of the “physical argument”

is a less theoretical physics, more of a practical mining thing which states

that for every ounce of gold mined there are only ten ounces of silver mined

(in fact it’s more like 9X, as this chart shows). It then goes on to say that

because there are only ten ounces of silver being put on the market for every

ounce of gold, their relative prices should reflect that comparative rarity.

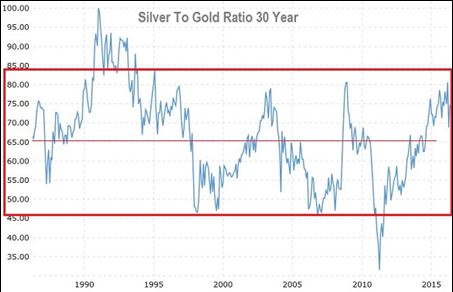

Those 9X or 10X or 16X ratios

between gold and silver compare to the above, the 30 year chart of the

silver/gold ratio shows the fluctuation and though the range is quite wide, if

we discount the couple of obvious outlier periods of the early 1990’s and then

the 2011 speculative peak on silver, it’s stayed inside the 46X to 84X range.

I’ve even dared to add in what I think is a fair best-fit average around the

65X level as over time, the ratio seems to revert to that mean. This 46X to 84X

range compares with the fundies/physics/geology-based counter-argument we saw

above and, say the most strident promoters of silver over gold (in fact they

tend to be silver over everything), that discrepancy shows the type of bright

future that silver has. Buy now, they say, before that 65X ratio goes to 16X.

By the way, if that 30 year

timescale isn’t enough of a sample for your taste and you want a longer period

that includes the US Gold Standard days, be my guest and play with the

macrotrends.net chart right here (2). But if you’re like me (or at least until

Doug Casey’s doom scenario for the USA and the world comes to pass) you’ll

probably want to base your anal ysis on the circumstances of the modern day

financial world. So, I go for the 30 year chart.

Anyway, back to the debate and with

the stage set, the crux of the issue why there should be such a large gap

between the relative prices of metals arguably 9X or 16X less common than one

another, as one gets to enjoy a price that’s 65X or 75X higher than its

stablemate. After all, both are what are known as “precious metals”, they come

from the same general area on the periodic table, a bucketful of either one is

very heavy, they’re both shiny, you can (and do) make and wear nice things made

of them, they’re both connected during human history to the concept of wealth

and money.

expensive than silver? Darned good question.

state that the gold/silver ratio is high because the market says it is high.

After all, 30 years (and longer) of a market willing to pay a 46X and 65X and

84X multiple for gold over silver isn’t something to be sniffed at, there must

be a good reason as to why gold gets that sort of premium. But that’s not a

solid case, it’s ultimately argumentum ad

lapidem (3)

because if

you adhere tightly to “that’s just the way things are” you don’t ban slavery,

women don’t get the vote, smoking tobacco isn’t seen as the health hazard it

is, etc. One of the things a natural-born contrarian (such as I) always looks for

is a market anomaly, something the world takes as read but ain’t necessarily

so, Joe. It is, after all, how the massive money was made in the 2008 subprime

crisis (see the movie The Big Short for more on that). But sadly I think in

this case the market is pricing silver to gold correctly, or at least fairly

correctly inside that wide-looking ratio range over the long-term and that our

dear and esteemed friend Keith Neumeyer is being at best disingenuous, most

likely plain ignorant, or perhaps just perhaps using the Greater Fool theory to

his own advantage because hell’s bells, there are some prize idiots in the

silverbug/goldbug world waiting to be harvested.

my argument for gold’s high relative valuation versus silver compared to its

physical availability.

Human

beings drool over gold like no other material. First and probably least important

we vertical, near-hairless monkeys like gold. There’s something about its colour,

feel and shiny heavy permanence that gets our animal hearts racing and it’s not

for nothing that the vast majority of the wedding bands in our wild and whacky

world are made out of the stuff (though not all, e.g. mine wasn’t). There’s an

emotional attachment to gold that just isn’t present in silver, even though we

like it well enough as a metal. As it can be found in native form, gold was one

of the first metals ever worked by human hand (if not the first), it has a

close connection with religions of all types, our relationship with gold goes

back untold years into pre-history. In short, we the animal and that metal have

a lot of collective baggage and that’s not something to discard lightly.

The

rarity premium. Second, as any economist will tell you there’s a rarity

premium that we are willing to pay. Put simply, I can pay U$5 for an ordinary

bottle of wine, U$50 for an excellent bottle that’s an obviously better

drinking experience than the vin ordinaire, then maybe U$500 for something that

scores 100 points and wins “Best Malbec of the Year” in Wine Magazine or

suchlike. That award winner isn’t ten times the experience of the excellent

bottle, but it’s almost certainly “better” and those with the type of

disposable income that doesn’t differentiate much between $50 and $500 will

snap them up. This opens the door to the other way in which items are priced at

higher multiples, the “social cachet” or “snob value” for items, for when

people feel the need to impress their peers.

In the case of gold, “rarity

premium” also comes with fundamental logic because way back when, it was far

easier to carry a lot of wealth in gold coins than it was in silver coins, pure

bulk determined that. There are still remnants of that today, e.g. the famous

occasion when Warren Buffett bought a very large position in silver, but then

sold in on quickly (in 2007 for a modest profit, but before the big lift-off in

the metal) when he realized how much the carry cost was for storing a large

monetary amount of silver. When you lived in 16th century Paris and

needed to pay for something very expensive in Florence, gold made far more

sense than silver.

Silver

is a quasi-commodity. Thirdly, we can now start to bring things up to date and make

some more progress to solving the GSR puzzle by noting that yes they’re both

shiny and make pretty jewelry, but in our modern world perhaps half of silver produced is used for

industrial purposes. Silver is a bit Jekyll and Hyde in that respect, it’s an

industrial commodity and a lot of it gets used and used up (it’s estimated that

a maximum of 10% of silver used in industry is recycle and even then the cycle

time is very long). And the same as any other industrial commodity, if it gets

too expensive demand becomes elastic and drops rapidly as alternatives are

found via innovation. Gold doesn’t have the same quasi-commodity status, there

is a slight market for gold in industry but to the vast majority it’s either

the raw material for jewelry (in itself a form of storage for an inelastic) or

it’s the monetary metal, the asset class, the store of wealth that gets dug up

out the ground, purified and then stuck back underground again (in vaults in Switzerland).

I once again bow to Paul van Eeden’s definition of gold when he calls it “the

very essence of money”. And he’s no permabull on the metal, either.

And before we move on, talking

about on silver’s industrial metal side reminds me of the last time I chewed

the cud deeply on silver prices, back in IKN320 dated June 28th 2015, when the subject was more about the

supposed manipulation of the silver price market. In the end I think silver is

somewhat manipulated, but only because every single capital market is also

manipulated by big money. The difference with silver is that 1) it’s small

enough to see the manip in action, it becomes pretty freakin’ blatant at times

and 2) as I wrote in IKN320, over half the customers for silver don’t care.

Back then I wrote…

end-hoarder, big difference) is going to kick up a fuss and complain about

artificially low silver prices? The masochist end of the silver market,

perhaps?”

then.

Silver

isn’t just cheaper to buy. So far we’ve considered theoreticals, historic and

cultural reasons. We’ve also considered modern-day demand, but the final piece

is in my opinion the most important driver of the modern relationship between

silver and gold and it’s from the supply side of the equation.

Silver isn’t just cheaper to buy,

it’s a lot cheaper to produce. It’s a tough call to give an exact figure

for the operating cash cost of producing one ounce of gold or one ounce of

silver. Even if we restrict ourselves to legal formal mines (and eschew all the

informal illegals with far lower costs in pure dollar terms) it’s difficult,

because “cash cost per ounce” is a classic of moving goalposts, there are

mining cash costs, operating cash costs, all-in sustaining cash costs, “All In”

cash costs, even “full enchilada” costs for a mining company that needs to

spend on exploration and development of future mines to offset the mined

ounces. There are protocols but there are no set laws and one company will-or-will-not

include this or that line item, things such as financing costs and and taxes

muddy the waters, any manner of other things.

So for argument’s sake, let’s go

for mine-only costs and let’s say they average at U$10/oz for silver and

U$800/oz for gold, which are the type of figures that stand up to reality over

the breadth of the silver and gold mining sector. You prefer 15 and 750? Or 12

and 600? All good with me but the point should be clear already, even at the

lowest ratio case above we are at a 50/1 cost ratio, 75/1 is easy enough to

imagine, 80/1 isn’t out of the question. It’s relatively very cheap to produce

an ounce of silver these days and that’s because the nature of silver mining

has changed radically in the last few decades. And yes, that 75/1 ratio does

look familiar all of a sudden.

The thing with silver is that its

supply dynamics have changed radically in the last 50 years or so. Long gone is

the image of the lonesome miner and his pick, left deep in the past are the

slaves of Potosí and veins of crazily high grading metal, these days most of

the world’s silver isn’t a product but a by-product. Or to quote a company that

really knows its beans when it comes to the metal, Silver Wheaton (SLW) (4):

silver production comes as a by-product from base metal and gold mines.”

examples, the 14Moz Ag annual from Antamina to name just one (and Antamina

recently received U$900m by selling a 33.75% stream of that to SLW). Those are

just fourteen million of the approximate 600m oz of silver that come from

by-product production of either base metals such as zinc and lead (with some

copper) or mines where yes indeed, it’s common to find silver atoms sitting

close to gold atoms in that 10:1 ratio the natural science people tell us

about. Development decisions, construction decisions and annual budgets at

these mines are not based on the price of silver. Yes silver’s price will help

or hinder the year at the mine in turn, but that’s as far at it goes. As long

as Mine X sells its zinc (or whatever) at the right price, that silver is going

to come out of the ground whether it’s wildly profitable or not.

The dedicated silver mining company

is a bit of a rarity these days, even more scarce is the silver miner that gets

most of its cash from its nameplate metal. First Majestic get around 80% of its

revenue from silver and that’s as good as they come, most silver miners are a

mix of metals and companies such as Fortuna (FVI.to) (FSM) or Pan American (PAA.to)

(PAAS) wouldn’t last two minutes without the cash that comes from the zinc,

lead and gold they sell. But even the “mixed” dedicated silver mines are a

rarity compared to the number of silver mine projects out there, because they

have to be able to run at a profit on silver alone and that means, above all,

they need to be the best end of the market with the highest grade or the lowest

running costs. Or both.

Tahoe Resources at Escobal is one

of a kind or, the other side of the coin, why isn’t the silver at Colquipucro

(TK.v) being mined yet and why has Tinka moved its flagship to the Ayawilca

zinc property? What about the 450m+ ounces of silver at the Levon Resources

(LVN) Cordero project in Mexico? For another, it’s under 43-101 compliance

there have been technical and economic reports galore and it has all its major

permits and is as “shovel ready” as you can imagine, so why isn’t Bear Creek

Mining’s (BCM.v) Corani project a working mine yet? Why isn’t it churning out

its 8m oz Ag per year? Answer: the silver price is too cheap to make any of

those work. Why so? Because a lot of other places can churn out silver and make

good money from the by-product.

There are literally dozens of low

grading silver projects out there in our strange world of junior mining capital

markets and they’d all work if silver were at U$25/oz. In fact, my thought

experiment would be to 1) watch silver spike to $25/oz then 2) buy out BCM.v and

buy long-dated calls and puts on silver to collar 8m oz of the metal at exactly

U$25/oz for the next 25 years then 3) finance and build the mine. They’d (We’d) raise

the cash easily once the finance people see the company had 100% rock-solid

guaranteed U$1.3Bn per year of topline revenues. It might screw the share price

totally and leave nothing for equity holders but hey…who cares? The

executives would get their salaries!

Silliness aside, what gold mining

companies bring to the table is specialty, to a large extent the formal

production of the world’s largest mining companies set supply. Gold’s pricing

is complicated because it reacts as a money, but I don’t think it’s much of a

coincidence that it settled at lows just under U$1,100/oz at the bottom of our

recently finished bear market where bottom line profits go to zero for the

majority. That doesn’t happen to the dedicated silver miners because price

discovery is totally out of their hands. The ones that make it are the ones

that show they can operate at the price set by the market and they’re the ones

that have a tight rein on costs, or high grade to offer margins, most likely

both. In the world of gold, if your timing to market is fortunate can get across

the capex hurdle and with a 0.5 g/t resource, you get to be a winner (Rio Alto

showed us that) as long as your costs are low. But 15X that grade would be a

7.5 g/t open pit silver mine…see many of those around you? Even double and a

30X Gold/Silver ratio at 15g? Or for another example, I’ve always been a fan of

the Ollachea gold project (definitely more than the mess of a company that owns

it) that may be only 3.4 g/t gold for an underground project, but I know the

costs parameters and economics work (and so does Cofide and, dammit and spit,

all the nasty scumball people trying to usurp it know too). You may get a

couple of silver mines running at 50X that ratio and 170 g/t Ag, but only as

long as they mine and process and sell enough zinc and lead by-products that

come out with the rock and even then, in today’s price environment they’re not

much more than breakeven (example Fortuna Silver at Caylloma). In the real

world, silver mines are limited by their margin because they don’t set the

market price, the near zero cost by-product ounces from the massive porpyhry,

skarn, IOCG etc production facilities around the world.

The bottom

line

We the retail mining investor still

have a reasonable shot at finding a real winner in the world of junior gold

explorecos and development companies because gold project tend to be masters of

their own fates. Once found and defined, they can stand alone and can hold up

to a low cost scenario but it’s far more difficult in the silver sub-sector to

find an equivalent economically robust project. It’s why the silver market

jumps through hoops for the rare ones like Tahoe’s Escobal, or puts high

valuations of the 44% of Valdecañas/Juanicipio development project owned by MAG

Silver, or gets hot and sweaty about discoveries like the recent and promising

Sandra Escobar discovery All three of those have (or are looking like having)

the killer combo of high grade and strong mining width and the silver market

goes loopy over them precisely because they’re very few and far between and

will attract the companies looking to be silver-centric.

At the same time, dedicated silver

miners are fighting the price discovery weighting of the producers of silver as

a by-product. They don’t have their livelihood at stake, the metal’s value is

useful without being vital, anything above cost of production is ultimately a

reasonable deal. As we’ve seen, market price of silver can be pushed to levels

below cost for the silver miners and the weight of by-product Ag is to blame.

The result is hundreds of millions of ounces of marginal silver ounces (all

supposedly economic if you believe those 43-101 reports) sitting on the

sidelines while their respective company officers light candles and pray to the

Market Gods for higher metal prices that are not going to happen, not in the

way they need, because marginal stays marginal as cost parameters rise with

metals prices.

But it’s the combination of four

factors, 1) near-religious human attraction for that special colour of shiny 2)

we way we pay extra for rare things 3) silver’s commodity factor 4) the cost

profile of producing silver, that result in a price ratio that’s much higher

than the “physical ratios” so loved by the silver salesmen and women. Yes we

can and may get a lower gold/silver ratio in the intermediate future (in the

range of that chart at least, we’re not seeing 15 to 1 ever again), yes the

charts have seen this particular squiggly line go up and down in the past but

there are absolutely no guarantees on the line moving down the way it’s done in

the past, not fundamentally-speaking at least. A world awash with by-product

keeps silver deposits sidelined and building up, any higher move releases the

Coranis of this world and supply cranks up quickly. There are far too many

marginal silver projects out there (and for that matter, precious few producers

that rise above the level of marginal or mediocre). When push comes to shove

and I demand quality from my junior exploreco or Rule 1 (make a profit) from my

small or medium-sized producer, gold options always outnumber those in the

silver space. And that’s where I will stay.