This was the main intro piece to this Sunday’s edition of the weekly.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

What gold has been doing and a guess as to why

“As above, so

below,

below,

as within, so without,

as the universe, so the

soul”

soul”

Hermes Trismegistus

First, a basic fact

about last week at the market; Our preferred ETFs for following the broad

spectrum of the PM sector and its companies all lost ground. The gold ETF GLD dropped 2.8%, the precious metals miner

ETF GDX dropped 2.1% and the junior miner ETF GLXJ dropped 1.3%. In other words

we’ve seen a correction going on in front of our eyes and as noted last weekend

when musing on its possibility in IKN374, that’s not a bad thing.

about last week at the market; Our preferred ETFs for following the broad

spectrum of the PM sector and its companies all lost ground. The gold ETF GLD dropped 2.8%, the precious metals miner

ETF GDX dropped 2.1% and the junior miner ETF GLXJ dropped 1.3%. In other words

we’ve seen a correction going on in front of our eyes and as noted last weekend

when musing on its possibility in IKN374, that’s not a bad thing.

Away from the world of gold permabears, that group of shining individuals

that make even the prepper end of the goldbug world look intelligent, it would

be tough to find a comment saying that what we saw last week was The Top and

it’s all going to go wrong for gold from here. But a correction it was, gold

backed off from the U$1,400/oz level very easily and its action reminded me

strongly of May 2016 and the sentiment at the time. Use charts, money-flow

data, group psychology studies or whatever you prefer, but the general consensus

in gold back in May was that gold’s move to $1.3k was “too much too soon” and

the metal needed another good reason to go higher before it could. We saw it

get oversold back to U$1,200/oz as well (and I even remembered a few of those

gold bears trying to raise their squeaky voices again right down at the bottom)

but we rebounded from that level too. Then came the Brexit event, a two stage

affair with sentiment pre-Brexit that showed growing fear of a Leave vote,

which waned the week before the vote took place. Then the big whammy on June 23rd

and the result day of June 24th, which shot gold through the

U$1,300/oz level with a vengeance. Since then it’s stayed there but as we’ve

seen in the last few days, it’s also dropped from highs.

that make even the prepper end of the goldbug world look intelligent, it would

be tough to find a comment saying that what we saw last week was The Top and

it’s all going to go wrong for gold from here. But a correction it was, gold

backed off from the U$1,400/oz level very easily and its action reminded me

strongly of May 2016 and the sentiment at the time. Use charts, money-flow

data, group psychology studies or whatever you prefer, but the general consensus

in gold back in May was that gold’s move to $1.3k was “too much too soon” and

the metal needed another good reason to go higher before it could. We saw it

get oversold back to U$1,200/oz as well (and I even remembered a few of those

gold bears trying to raise their squeaky voices again right down at the bottom)

but we rebounded from that level too. Then came the Brexit event, a two stage

affair with sentiment pre-Brexit that showed growing fear of a Leave vote,

which waned the week before the vote took place. Then the big whammy on June 23rd

and the result day of June 24th, which shot gold through the

U$1,300/oz level with a vengeance. Since then it’s stayed there but as we’ve

seen in the last few days, it’s also dropped from highs.

Okay, that’s the scenario to date. Now for a few statements mixed with a

few working theories to get us to a gold price forecast for the near future:

few working theories to get us to a gold price forecast for the near future:

1) Gold is bullish, period. It will take a lot more than a retrace from

U$1,380/oz to change that, so the “It didn’t break U$1,400/oz we all gonna die”

brigade can stick their whining where the sun doesn’t shine. This is the single

most important point, I urge you not to lose sight of the forest for the trees

and therefore repeat: Gold is bullish, period.

U$1,380/oz to change that, so the “It didn’t break U$1,400/oz we all gonna die”

brigade can stick their whining where the sun doesn’t shine. This is the single

most important point, I urge you not to lose sight of the forest for the trees

and therefore repeat: Gold is bullish, period.

2) The action in the last two months, from mid-May to today mid-July, has

been dominated by Brexit. The pre-vote sentiment that moved from one side to

the other and then back again, the big shock of a result the market wasn’t

expecting. And of course while we’re on the subject, count me in as I got my

call 100% wrong and was way too confident about a Remain result all the way

through the process (and being long the gold sector was one of my all-time best

“right for the wrong reasons” moments).

been dominated by Brexit. The pre-vote sentiment that moved from one side to

the other and then back again, the big shock of a result the market wasn’t

expecting. And of course while we’re on the subject, count me in as I got my

call 100% wrong and was way too confident about a Remain result all the way

through the process (and being long the gold sector was one of my all-time best

“right for the wrong reasons” moments).

3) It’s therefore no coincidence to see gold drop from its highs in the

same week in which “Brexit Fear” (or maybe that’s “Brexit Fear!!!”) abated on a

worldwide level. There’s plenty of financial sector evidence for that away from

the gold market, just look at the S&P hitting new highs or the way the

British Pound has reverted its drop (people calling “parity with Euro!” less

than a week ago have STFU en masse). The world has vaccinated itself against

Brexit fallout, the EU isn’t facing a new series of referenda (no sitting government

leader will be as stupid as David Cameron was, they tend to value their jobs)

and now it’s only a major headache for one small island sitting off the coast

of continental Europe. Over in the UK the appointment of a new Prime Minister

and her big ministerial re-shuffle has brought in a pro-Brexit team to lead the

Brexit talks, but even the top man among them David Davis talks about 2018 as

the earliest date to trigger the Article 50 leaving clause and that’s from the

most aggressive end of the pro-Brexiters in the new government. People, two

years is an eternity in the financial markets, it’s hardly a shadow on the

horizon but even then, the way in which the new PM has played the Scotland card

(1) (quite brilliantly if you ask me) means even 2018 looks too close for any

formal Brexit negotiations to start with the EU. I could go on and on about

this so I won’t, the bottom line is that Brexit Fear has all-but disappeared

under the new reality of “two years minimum” (and it’s a fair bet Brexit will

never happen).

same week in which “Brexit Fear” (or maybe that’s “Brexit Fear!!!”) abated on a

worldwide level. There’s plenty of financial sector evidence for that away from

the gold market, just look at the S&P hitting new highs or the way the

British Pound has reverted its drop (people calling “parity with Euro!” less

than a week ago have STFU en masse). The world has vaccinated itself against

Brexit fallout, the EU isn’t facing a new series of referenda (no sitting government

leader will be as stupid as David Cameron was, they tend to value their jobs)

and now it’s only a major headache for one small island sitting off the coast

of continental Europe. Over in the UK the appointment of a new Prime Minister

and her big ministerial re-shuffle has brought in a pro-Brexit team to lead the

Brexit talks, but even the top man among them David Davis talks about 2018 as

the earliest date to trigger the Article 50 leaving clause and that’s from the

most aggressive end of the pro-Brexiters in the new government. People, two

years is an eternity in the financial markets, it’s hardly a shadow on the

horizon but even then, the way in which the new PM has played the Scotland card

(1) (quite brilliantly if you ask me) means even 2018 looks too close for any

formal Brexit negotiations to start with the EU. I could go on and on about

this so I won’t, the bottom line is that Brexit Fear has all-but disappeared

under the new reality of “two years minimum” (and it’s a fair bet Brexit will

never happen).

4) In a bull run in any issue, large or small, asset or equity, we’d want

to see exactly the type of pulse-retrace-pulse we’ve seen this year in gold.

Discount the trend-breaking moment in February (clear as a bell in hindsight)

and considering March to July 17th, the way the gold price has moved

has been obviously and clearly bullish, you couldn’t ask for more. Well, you

could if you’re one of those “Wheee To Da Moon Alice” people but here at The

IKN Weekly we prefer to hold on to our profits after making them.

to see exactly the type of pulse-retrace-pulse we’ve seen this year in gold.

Discount the trend-breaking moment in February (clear as a bell in hindsight)

and considering March to July 17th, the way the gold price has moved

has been obviously and clearly bullish, you couldn’t ask for more. Well, you

could if you’re one of those “Wheee To Da Moon Alice” people but here at The

IKN Weekly we prefer to hold on to our profits after making them.

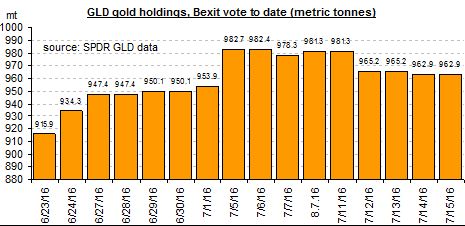

5) The hot speculative money washing through gold that I mentioned in

last week’s opener showed itself again in no uncertain terms. Here’s an update

of the GLD bullion inventory chart of last week, Brexit-to-date, and look how

nearly 20 tonnes was taken off the top of holdings last week, 16 of them in one

shot. That’s not the type of action you get from people wanting to protect

their asset value with a long-term position in the world’s historic keystone

store of wealth.

last week’s opener showed itself again in no uncertain terms. Here’s an update

of the GLD bullion inventory chart of last week, Brexit-to-date, and look how

nearly 20 tonnes was taken off the top of holdings last week, 16 of them in one

shot. That’s not the type of action you get from people wanting to protect

their asset value with a long-term position in the world’s historic keystone

store of wealth.

In the great scheme of things, 20 tonnes of gold is neither here nor

there but in the short-term, particularly in the current strange days, it

matters.

there but in the short-term, particularly in the current strange days, it

matters.

Bottom line: Putting all those bits together, unless a new event comes along to

justify a new move in the price of gold we’re going to be stuck where we are

for a while and will probably see it move back to U$1,300/oz, too. And before

you say anything under your breath, sorry Turkey and its attempted coup this

weekend doesn’t count, we’ve already seen a dozen geopolitical events come and

go (Greece, Cyprus, Ukraine, Israel, ISIS, Syria etc etc), they all threaten to

destabilize EVERYTHING for a while and then they don’t. The reason Brexit has

been different (or if you like, affected gold for a couple of weeks rather than

a couple of days) is that it had (has?) a direct world-scale financial effect,

not just a political one. Summed up, Brexit shot gold higher because the world

was afraid of Brexit. Now the world isn’t afraid any more. What goes up comes

down, Hermes said so. On the other hand gold stocks have two modes of impetus, not

just one. The money now moving into the sector is more than enough to make for

a vibrant bullish market even if gold consolidates for a while, so I fully

expect the good times to keep rolling for the gold stocks even if the

underlying metal treads water a while. I own gold, I trade stocks. Two

different things.

justify a new move in the price of gold we’re going to be stuck where we are

for a while and will probably see it move back to U$1,300/oz, too. And before

you say anything under your breath, sorry Turkey and its attempted coup this

weekend doesn’t count, we’ve already seen a dozen geopolitical events come and

go (Greece, Cyprus, Ukraine, Israel, ISIS, Syria etc etc), they all threaten to

destabilize EVERYTHING for a while and then they don’t. The reason Brexit has

been different (or if you like, affected gold for a couple of weeks rather than

a couple of days) is that it had (has?) a direct world-scale financial effect,

not just a political one. Summed up, Brexit shot gold higher because the world

was afraid of Brexit. Now the world isn’t afraid any more. What goes up comes

down, Hermes said so. On the other hand gold stocks have two modes of impetus, not

just one. The money now moving into the sector is more than enough to make for

a vibrant bullish market even if gold consolidates for a while, so I fully

expect the good times to keep rolling for the gold stocks even if the

underlying metal treads water a while. I own gold, I trade stocks. Two

different things.

That’s enough for one day but before we move on, please note the use of

the word “guess” in the title line of this intro piece. I’m under no illusions

and I’ve been wrong along the way in 2016 too, this may be another one of those

moments. I’ve had to keep questioning my attitude towards gold (market leader

it is) and the mining stocks. As an example see my bad Brexit Remain call above,

for another please recall the way I fixated on gold re-tracing back to

U$1,180/oz in March and lost a few good entry points on stocks as a result. I

finally got that out of my system in IKN361 dated April 10th (before

too much damage was done). Today’s piece can be summed up by “near term gold

sideways and stocks bullish” but it’s just another working theory, subject to

change and so forth.

the word “guess” in the title line of this intro piece. I’m under no illusions

and I’ve been wrong along the way in 2016 too, this may be another one of those

moments. I’ve had to keep questioning my attitude towards gold (market leader

it is) and the mining stocks. As an example see my bad Brexit Remain call above,

for another please recall the way I fixated on gold re-tracing back to

U$1,180/oz in March and lost a few good entry points on stocks as a result. I

finally got that out of my system in IKN361 dated April 10th (before

too much damage was done). Today’s piece can be summed up by “near term gold

sideways and stocks bullish” but it’s just another working theory, subject to

change and so forth.